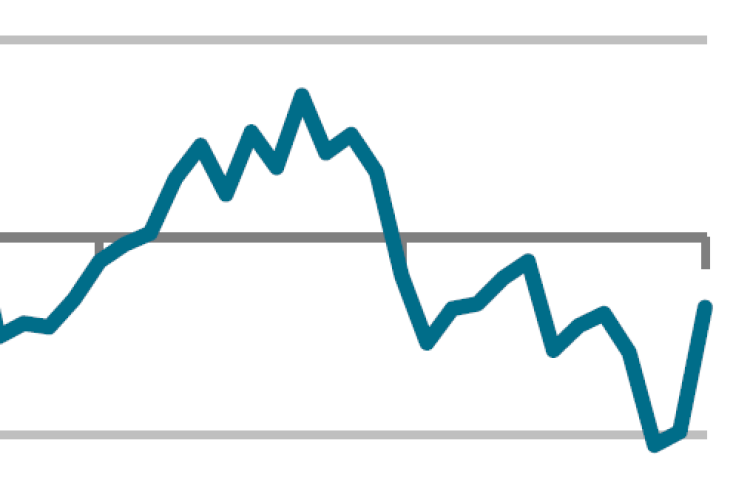

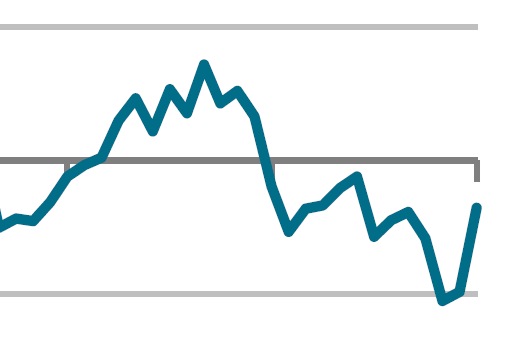

January data indicated a much slower decline in construction output than at the end of 2025.

At 46.4 in January, the seasonally adjusted S&P Global UK Construction Purchasing Managers’ Index (PMI) was up sharply from December’s five-and-a-half year low of 40.1.

All three sub-sectors recorded weaker rates of contraction than those seen in December, helped by a more stable demand environment and reports of a gradual turnaround in sales pipelines.

However, inflation appears to be on the rise again, inhibiting construction purchasing activity.

The January PMI was the highest since June 2025, but below the 50.0 no-change value for the 13th month in a row, and indicating another solid reduction in total industry activity.

House-building was the weakest-performing segment in January (index at 39.3), though the pace of contraction eased to its slowest for three months. Survey respondents cited a lack of new residential development projects and subdued demand conditions. Civil engineering activity also decreased at a sharp pace in January (40.6). But the latest fall in commercial work (48.4) was the slowest since May 2025. Some firms suggested that post-budget clarity and improved investor sentiment had helped to stabilise demand in the commercial segment.

Total new work also decreased but to the least marked extent for three months. Where order books deteriorated, this was often attributed to risk aversion and fragile confidence among clients (especially in the housing segment). However, there were some reports of a turnaround in public sector work and sales enquiries for commercial projects at the start of 2026.

Business activity expectations for the year ahead continued to rebound from the 35-month low seen last November. Around 38% of the survey panel predict a rise in output volumes during the next 12 months, while 17% foresee a reduction. The resulting index pointed to the highest level of optimism since May 2025, although confidence was still well below the long-run survey average. Anecdotal evidence cited lower borrowing costs, greater infrastructure spending and hopes of a recovery in housing market activity as factors likely to support construction workloads.

Meanwhile, a robust and accelerated increase in average cost burdens presented a challenge for construction companies in January. The overall rate of input price inflation was the fastest since last September. Survey respondents noted that suppliers had passed on higher raw material and wage costs. Subcontractor charges also increased at a solid pace, despite the sustained downturn in demand.

Squeezed margins and subdued order books weighed on construction employment. Latest data signalled another reduction in staffing numbers, extending the current period of job losses to 13 months.

Against this background, purchasing activity decreased sharply. January cutbacks mostly reflected a lack of new work to replace completed projects.

Tim Moore, economics director at S&P Global Market Intelligence, which compiles the survey, said: “January data provided encouraging signs that the UK construction sector has exited its tailspin, and firms are becoming more hopeful that new projects will get back on track in 2026.

“The latest reduction in total industry activity was the slowest since last June. Commercial work outperformed, with activity moving close to stabilisation amid a post-budget boost to contract awards. House building weakness persisted, although even here the rate of decline eased considerably since December and was the least marked for three months.

“Construction companies noted subdued underlying demand due to fragile client confidence and elevated risk aversion, but there were some reports of improving investment sentiment and greater sales enquiries at the start of the year. As a result, business activity expectations rebounded to an eight-month high, while the pace of job losses moderated.

“Supply conditions improved again in January. Lead times for the delivery of construction items shortened for the sixth month in a row and subcontractor availability increased at a solid pace. However, margins were under pressure as higher wages and raw material prices led to the sharpest rise in purchasing costs since September 2025.”

Brian Smith, head of cost management at Aecom, said: “A second consecutive month of slowing decline suggests that the market could be climbing out of its slump and contractors can see brighter days ahead.

“We know from our latest London Main Contractor Survey that confidence in the capital at least will remain low for the short-term, but we’re seeing a healthy level of competition in the market and order books are nearing capacity for 2026.

“What will dictate when the market makes a full recovery is clients’ ability to move forward with projects. Tender prices are rising, as contractors pass on labour and material costs, and sticky inflation means that interest rates aren’t being cut as quickly as some may have hoped.

“Ultimately, accelerating delivery, finding innovative ways to boost competitiveness and diversifying projects taken on are the hallmarks of a confident contractor this year.”

Got a story? Email [email protected]