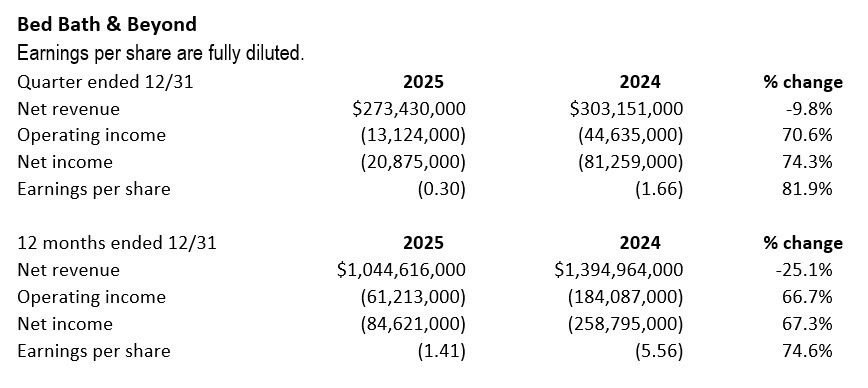

MURRAY, Utah — Revenue is still declining for Bed Bath & Beyond Inc., but at a slower rate, edging the company toward profitability, according to its fourth quarter earnings report.

The operator of retailers Bed Bath & Beyond, Overstock, Buybuy BABY and Kirkland’s Home, along with a blockchain asset portfolio, delivered its eighth consecutive quarter of improvement. Revenue for Q4 was $273 million, which represents a 9.8% year-over-year decrease. Excluding its exit from Canada, revenue declined 6.4% year-over-year. For the full year, revenue fell by 25.1%.

“We saw the rate of revenue decline compress meaningfully throughout the year,” said Marcus Lemonis, executive chairman and CEO, “positioning us for a return to top-line growth. Our fourth quarter capped a year of measurable financial and operational progress. We built our core retail discipline, improved margins, enhanced marketing efficiency and strengthened our balance sheet,” he said.

See also:

- Wedbush is bullish on Bed Bath & Beyond—here’s why

- Former Walmart exec tapped for Bed Bath & Beyond leadership team

“Revenue remains a key priority with focused effort on conversion and retention tactics to drive disciplined growth,” said Adrianne Lee, president and CFO. “We are encouraged by the significant narrowing of net loss, adjusted EBITDA loss and operating cash flow use we achieved in 2025.

“2025 was about stabilizing and building the base of our business,” he said during the company’s earnings call. Lemonis emphasized that the company made a deliberate decision to eliminate vendors and SKUs that generated negative margin contribution. “We chose margin integrity over headline revenue.”

Gross profit for the quarter was $67 million, or 24.6% of net revenue, which was an improvement of 160 basis points vs. the same quarter in 2024. Sales and marketing expense was $38 million, or 13.8% of net revenue. The company’s technology and administrative expenses declined to $33 million from $48 million in the prior year’s Q4.

For the fourth quarter, net loss was $21 million, a $60 million improvement year-over-year. Adjusted EBITDA was $4 million, up $23 million year-over-year.

For the full year, net revenue was $1 billion, down 25.1% over 2024. Excluding the impact of exiting Canada, the year’s revenue decline was 21.6%. Gross profit for 2025 was $258 million, or 24.7% of net revenue, while sales and marketing expense was $143 million, or 13.7% of net revenue.

Net loss narrowed to $85 million, an improvement of $174 million year-over-year. Adjusted non-GAAP EBITDA loss was $31 million.

The company’s outlook for 2026 is for revenue trends to continue to improve, targeting low- to mid-single digit topline growth for the full year. Growth is expected to be driven by improved conversion, higher order value, enhanced retention efforts and expanding ecosystem capabilities.

Lemonis told analysts on the call that the company expects year-over-year revenue growth in the 30% range vs. the previous year in Q1 2026. In the second quarter, with the closing of the Kirkland’s acquisition on or around April 1, the company will focus on 90 to 120 days of integration activity, which will accrue transaction costs. When the integration is completed, he said, Q3 should see positive top line growth with the objective of breaking even, before heading into Q4 and an “opportunity for profitability.”