While geopolitical headlines have captured the market’s attention more recently, 2026 has also been marked by widespread AI disruption fears.

As frontier labs like Anthropic have released more advanced AI tools and models, markets have begun to reprice the risk that certain businesses face as AI threatens their business model.

During the first quarter, this market trend had an outsized impact on technology stocks, however it has also affected other service-based businesses like insurance, wealth management and even private credit firms.

What happened next is the part worth paying attention to.

As capital fled AI-exposed equities, it moved — quietly but deliberately — into commercial real estate and other asset-heavy sectors perceived to be more immune from AI disruption.

In the first quarter, global and U.S. REITs (Real Estate Investment Trusts) returned 1.3 per cent (USD) and 4.8 per cent (USD) respectively, while the S&P 500 fell -4.4 per cent (USD).

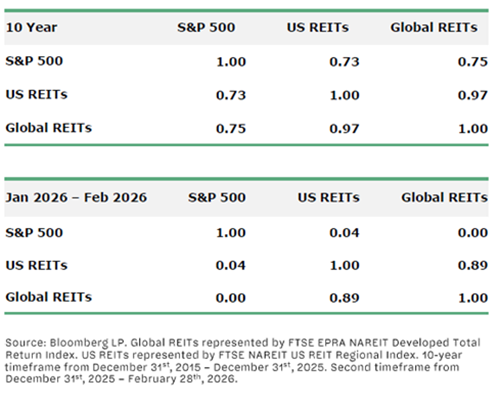

More telling is the correlation data: over the past decade, global and U.S. REITs have demonstrated correlations of 0.75 and 0.73 with the S&P 500. However, in the first two months of 2026 (before geopolitical escalations in March), those figures dropped to near zero.

REIT Correlation Matrix Comparison:

This dynamic, described as the “AI immunity trade,” reflects a clear market preference for businesses with heavy physical assets, durable economic relevance and barriers to entry that no algorithm can replicate.

Utilities, energy and real estate are among the sectors that fit this description. The logic is not that businesses in these industries are technology-resistant — it is that they offer something AI genuinely cannot substitute.

Three key structural qualities make REITs uniquely resistant to fundamental AI displacement risk. All three are directly relevant to the people who build commercial real estate.

The first quality is the contractual nature of real estate cash flows. REIT leases are long-term, with rent escalators and structural default protections baked in. As a result, a REIT operator’s rent roll is insulated from technology replacement risk which can sink a software company.

The second is physical scarcity. You cannot build a new logistics hub where there is insufficient land.

You cannot build a new data centre where there is no power availability. You cannot build a mid-rise residential development without zoning approvals, skilled trades workers and construction timelines that span years.

AI can improve certain parts of the real estate value chain, but it cannot eliminate fundamental supply constraints. The very constraints that make construction time-consuming are exactly what make the finished product scarce and, ultimately, valuable.

The third key quality that makes REITs more immune to fundamental AI replacement risk is non-digital demand.

Warehouses hold inventory. Data centres house servers. Multifamily REITs provide homes for people to live in, and of the strength of a retail shopping centre is location dependent. These functions are physical by definition. They cannot be digitized away.

The most direct story for the construction sector, though, is not that AI cannot replace buildings. It is that AI actively requires them to be built.

The hyperscalers — Microsoft, Google, Amazon and their counterparts — are projected to spend over $660 billion (USD) on data centre infrastructure this year alone. This unprecedented capex has been a tailwind for data centre REITs.

That performance is not driven by financial engineering. It reflects a physical infrastructure buildout that requires poured concrete, high-voltage electrical systems, precision cooling, structural steel and millions of square feet of purpose-built space.

Someone has to build all of that.

Conversations about AI in construction often focus on automation risk: AI-assisted estimating, generative design tools, autonomous equipment.

Some of these will change workflows and some already have but construction management, skilled trades and site supervision require physical co-ordination, contextual judgment and on-the-ground problem-solving that remain genuinely difficult to automate.

What the AI immunity trade ultimately tells us is that investors have started pricing-in AI disruption risk more than ever before and companies whose value depends on physical assets that take years to construct cannot be replaced by a model update.

Construction also plays an important role as the demand pipeline for AI infrastructure is not going away soon.

Samuel Sahn is managing partner and portfolio manager at Hazelview Investments, a global real estate investment firm. He is co-author of The AI Immunity Trade and REITs. Send Industry Perspectives Op-Ed comments and column ideas to [email protected].